Non dico che non si debba cavalcare da un punto di vista speculativo la ri-salita dei prezzi immobiliari made in USA (non a caso anticipai con ottimo timing il bottom dei prezzi nell'estate 2011...ma non riuscimmo ad organizzare un Gruppo d'Acquisto come su Berlino)

Non dico che non si debba cavalcare da un punto di vista speculativo la ri-salita dei prezzi immobiliari made in USA (non a caso anticipai con ottimo timing il bottom dei prezzi nell'estate 2011...ma non riuscimmo ad organizzare un Gruppo d'Acquisto come su Berlino)...però sul fatto che in USA ci sia una RIPRESA IMMOBILIARE a tutti gli effetti e sulla base di solidi fondamentali sussistono forti dubbi.

Anche in questo caso il QE-rumore di fondo della FED confonde assai....

E' stata dura...

ma finalmente ho trovato un'analisi fuori dal coro che conferma i MIEI DUBBI sulla cosiddetta ripresa immobiliare americana (o se preferite sul ri-gonfiaggio della bolla immobiliare).

Infatti nei canali mainstream si trova solo "propaganda" e titoloni del tipo: nel mese xxx maggiore incremento prezzi case USA dal 2006, segno che la Ripresa si rafforza...etc etc

Non a caso anche il migliore esperto immobiliare americano

ovvero il Blogger Calculated Risk

(che ha perfettamente anticipato il bottom dei prezzi immobiliari USA e la conseguente ripresa)

nutre qualche dubbio ed esitazione.

Existing Home Inventory is up 16.4% year-to-date on May 27thPoi quel solito cattivello di Zero Hedge si chiede come possa esserci una VERA Ripresa immobiliare in USA senza un boom del prezzo del Lumber (legname) e senza servirsi di architetti...;-)

One of key questions for 2013 is Will Housing inventory bottom this year?.

Since this is a very important question, I'm tracking inventory weekly in 2013.

...Once inventory starts to increase (more than seasonal), buyer urgency will wane, and I expect price increases to slow....

The Housing UnRecovery Is Here: Architectural Billings Plunge Most Since 2008Io invece già espressi la mia visione nei seguenti post:

by Tyler Durden on 05/24/2013

Not only is this 'housing recovery' being built without the use of Lumber (as we explained here), but Architects are no longer useful either. The last two months - as homebuilder stocks surge and house prices spike - has seenArchitectural billings plunge by the most since November 2008. The current level of activity is at its lowest since June 2012 - hardly indicative of the rampaging rapacious demand for homes that we are spoon-fed day after day...

- La Bolla Immobiliare USA si sta ri-gonfiando molto rapidamente

- Immobiliare USA: la spintarella di Ben...

Ed ecco l'analisi a cui facevo riferimento ad inizio post. ..............

.

L'INFORMAZIONE INDIPENDENTE NON GODE DEL PRIVILEGIO DEI SUSSIDI STATALI.

CLICCATE SUI VIDEO PUBBLICITARI

Fondamentalmente si sposa con la mia tesi

ovvero che la maggior parte della mitica ripresa immobiliare made in USA è effetto del pompaggio della FED e del ri-gonfiaggio delle varie BOLLE che erano esplose nel 2008-2009.

Pertanto Hedge Funds, Fondi di Private Equity, Fondi Immobiliari etc si buttano a pesce a comprare casette made in USA facendo lievitare i prezzi in una versione immobiliare del Don't Fight the FED o meglio dell'investi sulle mosse della FED: da 4 anni è il miglior metodo per fare trading su qualunque assets...

Non ho il tempo di tradurlo, sorry.

Ecco qua e leggetelo con attenzione:

Housing Prices Are Being Dangerously Distorted by Big Institutional Money

The airwaves are full of stories of economic recovery.

One trumpeted recently has been the rapid recovery in housing, at least as measured in prices.

The problem is, a good portion of the rebound in house prices in many markets has less to do with renewed optimism, new jobs, and rising wages, and more to do with big money investors fueled by the ultra-cheap money policies of the Fed.

On my recent trip to Salt Lake City, Utah, after presenting to a bi-partisan audience in the Capitol building, a gentleman came up to me and introduced himself as a real estate agent.

He explained that he'd been seeing something very strange over the past six months, where very well capitalized, out-of-state private equity funds had been buying up huge swaths of residential real estate with cash. He wanted to know if I knew anything about this.

Of course I had been tracking this phenomenon for a while.

But I had not been aware that Salt Lake City had been one of the targets, so I asked him how the deals worked there.

Apparently, the hedge funds make "full ask" price offers, sight unseen and without conditions (such as inspections and the like), for whole baskets of available properties, typically in the middle to lower price ranges.

The effect, not surprisingly, is that regular home buyers are being outbid and eventually priced out of the market.

Over time, these full cash offers at the ask get noticed and home sellers begin to raise their asking prices.

For a young family saving to obtain the required 20% down, a 10% hike in price on a median house translates into an additional $3k - $4k that they must have to set aside to make the deal work (assuming they've not just been priced out of the house they wanted to buy).

The impact, he told me, is that a growing number of young families are finding themselves unable to obtain their first home.

They can thank Ben Bernanke for this. Here's why.

The Back Story

The housing propaganda machine has been turned on in full force, as exemplified by this article in the Wall Street Journal that headlined the front page:

There you have it.Home Sales Power Optimism

May 28, 2013

Home prices surged during the first quarter at their fastest pace in nearly seven years, the latest sign of a sustained warm-up in an economic recovery that has otherwise been marked by starts and stops.

The housing-market revival—and an accompanying report on consumer confidence—adds new grist for a debate inside the Federal Reserve about how far to push its easy-money policies, including an $85 billion-a-month bond-buying program which has helped to keep mortgage rates near historic lows, boosted asset prices and begun to stimulate hiring and spending.

Over the past year, the share of foreclosed property sales has fallen, particularly in California cities, Las Vegas, and Phoenix, which have posted the largest year-on-year price growth

The latest reports were big factors driving financial markets Tuesday. Stock investors, encouraged by the strong data, sent the Dow Jones Industrial Average to a new high.

The rising house prices are being presented as a signal of a "sustained economic recovery" that feeds into consumer confidence and as reason to propel the stock market to new all-time highs.

What's not to like in that narrative?

However, if you value context, the above article will leave you disappointed because it omits the main driver of house price gains in the areas mentioned: big, institutional money seeking rental income and future capital gains.

As the article noted:

Many of the largest home-price gains have come in the West, including many markets hit hardest by the foreclosure crisis.The fact that big funds with big money have been very aggressive cash buyers in the formerly hardest-hit markets is very well documented and has been for well over a year.

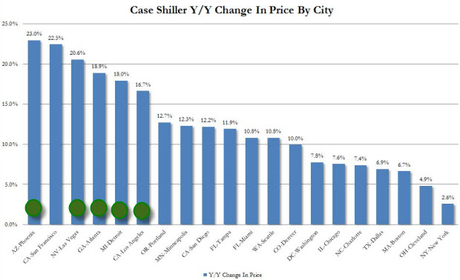

In March, prices were up by 22.5% in Phoenix from one year earlier, and by 22.2% in San Francisco. Other cities with double-digit gains included Las Vegas (20.6%); Atlanta (19.1%); Detroit (18.5%); Los Angeles (16.6%); Portland, Ore. (12.8%); Minneapolis (12.5%); San Diego (12.1%); Tampa, Fla. (11.8%); Miami (10.7%); and Seattle (10.6%).

How such important context gets left entirely out of an article about house-price appreciation in exactly those same markets is something of a mystery, at least from the standpoint of honest journalism.

Here's just one article out of many that have observed and reported on this issue:

With up to 30% of all home sales in some markets going to funds that have been notable for buying with cash at the asking price, it is not hard to conclude that the big funds are driving up prices.Wall Street Institutions Behind Home Price Surges in Markets Like Phoenix

Mar 18, 2013

The March MarketPulse report from CoreLogic examines the rise of institutional investors and the effects they are having on distressed inventory. The analysis, compiled by CoreLogic deputy chief economist Sam Khater, looked at 16 major U.S. housing markets where bank-owned inventory (REOs) have been relatively high since the housing bubble burst.

He assessed whether local activity was comprised of mom-and-pop individual investors or institutional investors, defined as either entities that have purchased five-plus properties a year under the same name or under an incorporated name.

Here’s what Khater found: institutional investors have been targeting specific markets and then accelerating purchases of REOs in those markets, driving down distressed inventories and leading to notable increases in REO prices that have in turn led to larger market uptick..............

A simple comparison of the Case-Schiller Index, which the media trumpeted as revealing that housing has recovered with the list of areas where the big money funds have been most active, shows (noted by green circles over the blue bars) the following:

That is, the places where the biggest price increases have been noted are the same places that giant institutional funds are buying up tens of thousands of properties at the ask.

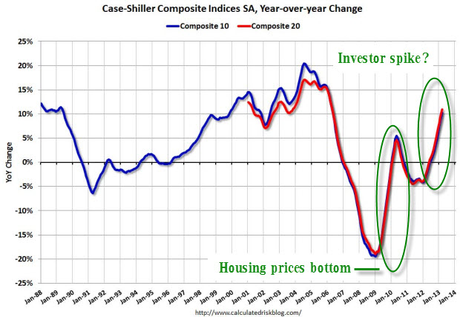

Where the first 'rebound' seen after a market correction is the prices of the asset merely stabilizing (because the yr/yr comparisons eventually head to zero), the most recent gains are definitely at levels that have been associated with bubbles and eventual corrections.

(Source)

Here are a few more articles for context, each of which demonstrates the obvious impact of institutional money on various key housing markets:

Hedge funds crowd first-time buyers out of housing market

Dec 10, 2012

There are still a whole lot of foreclosed houses out there. You would think that means it's a great time for first-time buyers to purchase a house. But that's not the case: One reason, private equity firms are buying up huge numbers of single-family houses. Wall Street wants to turn them into rentals.

Jonathan Shidler is a realtor in California.

Lately he gets at least one call every day from a hedge fund manager who wants to buy single-family houses in bulk.

He says they are buying them like a financial instrument, "which is fine and dandy. But what's different about these instruments is people live in them...........

In the past twelve months, Blackstone has raised over $8 billion to buy up medium- and low-priced housing, while JP Morgan has initiated a fund to buy up to 5,000 homes. Morgan Stanley has raised a billion dollars to buy up to 10,000 homes.Blackstone Buys Atlanta Homes in Largest Rental Trade

Apr 25, 2013

Blackstone Group LP (BX) bought 1,400 properties in Atlanta, some eligible for federal low-income housing subsidies, in the biggest bulk purchase for the fledgling homes-for-lease industry.

The private-equity firm, which has spent more than $4 billion on 24,000 rental properties in the last year making it the largest buyer in the U.S., purchased the residences from Building and Land Technology, said Marcus Ridgway, chief operating officer of Invitation Homes, Blackstone’s single- family rental division.

If it strikes you as odd that the big banks would be bailed out by the taxpayers and then turn around and use that same money to buy homes to then rent back to those same taxpayers, then we hold the same view.

This trend has been running for so long, and it is so obvious, that it really raises a very important question as to exactly how such context can be left out of any article on the recent rebound in house prices.

As we saw with bonds being driven to generational lows, the Fed's distorting buying habits shaped the prices for the entire bond market, ranging from Treasurys to corporate junk.

Nobody in their right mind would ever consider the prices of bonds to be telling us anything useful about risk, reward, the future, or even current conditions without noting that their current prices are heavily manipulated to the upside.

Similarly, the stock market is clearly being driven upwards on a sea of Fed-supplied liquidity, and everybody knows that once if that Fed money dried up today, the stock market would fall like a stone.

Housing is no different.

As big as the market is, prices are driven at the margins, and the buying pressure of institutional money snapping up thousands and thousands of properties in a single market in a single month means that this money, too, is having a distorting effect and is driving prices upwards.

Unfortunately, it seems like the lessons of 2008 went entirely unlearned.

Conclusion (to Part I)

It seems entirely wrong that the Fed bailed out big banks and made money excessively cheap for institutions, and that this is being used to price ordinary people out of the housing market.

Said another way, the Fed prints fake money out of thin air, and some companies use that same money to buy real things like houses and then rent them out to real people trying to live real lives.

In Part II: And the Smart Money is Already Withdrawing, we examine the growing pile of data warning that we are re-entering bubble territory in a number of housing markets.

At the same time, we are also beginning to see the very same hedge funds that have re-inflated these prices slink out of the market now that the party is kicking into higher gear – all while new buyers are increasingly having to abandon prudence to buy into markets where the fundamentals simply aren't there to merit it.

Didn't we just learn a few short years ago how this all ends?

Click here to read Part II of this report

.

CLICCA SULL'ICONA DELLA MOSCA TZE-TZE E VOTA PER QUESTO POST!

.

Se trovate questo post interessante, siete invitati a condividerlo con i tasti "social" (Facebook, Twitter etc) che trovate subito dopo la fine del testo.

Sostieni l'informazione indipendente e di qualità